Pocketly Loan App Safe or Not – From coaching fees in institutions to daily expenses, subscriptions, gadgets, and the occasional “bhai party deni hai” moments… money disappears faster than expected. And when savings run dry, apps like Pocketly suddenly look like a lifesaver.

But here’s the real question:

Is Pocketly actually safe for students, or just another trap with hidden risks?

I’ve seen friends use it, tested similar apps myself, and even had a small “repayment panic” phase once. So in this article, I’ll break everything down in simple terms—no jargon, no sugarcoating.

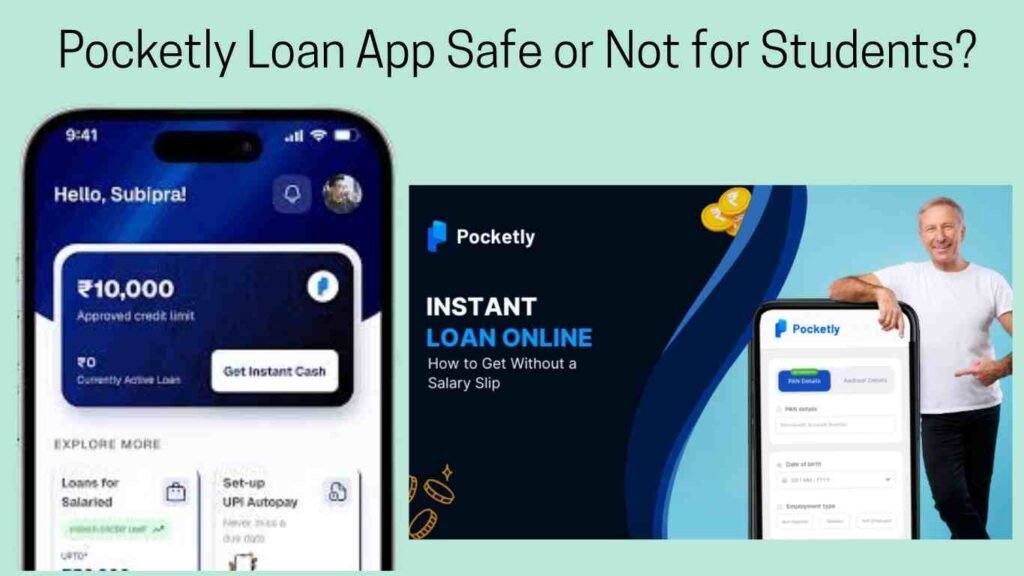

What is Pocketly Loan App?

Pocketly is a small personal loan app designed mainly for students and young users in India.

You can borrow small amounts like ₹1,000 to ₹25,000 quickly using just your smartphone. No long paperwork, no bank visits.

Key Features:

- Instant loan approval (within minutes)

- Minimal documents (PAN, Aadhaar)

- Designed for students & first-time borrowers

- Short repayment period (7–30 days typically)

Sounds perfect, right? But the reality has more layers.

How Pocketly Works (Simple Breakdown)

Here’s how most students use it:

- Download the app

- Enter basic details (name, college, income if any)

- Upload PAN & Aadhaar

- Loan gets approved

- Money credited to bank account

The process is smooth. Too smooth sometimes.

That’s where caution should start.

Is Pocketly Safe for Students?

✔️ The Short Answer:

Yes, but only if used very carefully.

✔️ The Real Answer:

It is not a scam, but it can become risky if you don’t understand the costs and pressure behind it.

Let’s break both sides.

👍 Why Students Use Pocketly (The Good Side)

1. Instant Money in Emergencies

Let’s say:

- Your laptop stops working before exams

- You need to pay hostel fees urgently

- Or you’re stuck without cash at the end of the month

Pocketly can genuinely help in such situations.

2. No Income Proof Needed

Most banks reject students because:

- No salary

- No credit history

Pocketly fills that gap.

3. Helps Build Credit Score

If you repay on time:

- Your CIBIL score improves

- Future loans become easier

This is actually a smart move if used responsibly.

⚠️ The Risks You Should NOT Ignore

Now comes the part many influencers won’t tell you.

1. High Interest & Hidden Charges

At first glance, interest looks small.

But when you calculate properly:

- Processing fee

- GST

- Late fees

👉 The effective cost becomes quite high.

Example:

- Loan: ₹5,000

- You may receive: ~₹4,500

- Repay: ₹5,500 or more

That’s a big difference.

2. Very Short Repayment Time

Most loans are for:

- 7 days

- 14 days

- 30 days

For students with no steady income, this is stressful.

3. Harassment Risk (If You Miss Payment)

This is where things get serious.

Some users report:

- Continuous calls

- WhatsApp reminders

- Pressure tactics

Not always extreme, but definitely uncomfortable.

4. Data Access Concerns

Like many loan apps, it may ask permission for:

- Contacts

- SMS

Even if used for verification, it still feels intrusive.

Comparison: Pocketly vs Traditional Student Loans

| Feature | Pocketly App | Bank Student Loan |

|---|---|---|

| Approval Speed | Instant | 3–10 days |

| Documentation | Minimal | Heavy paperwork |

| Interest Rate | High (effective) | Lower |

| Loan Amount | Small (₹1k–₹25k) | Large (₹50k–₹10L) |

| Repayment Time | Very short | Long-term |

| Risk Level | Medium–High | Low |

👉 Conclusion: Pocketly is for short-term emergencies, not long-term financial planning.

Real-Life Example (Relatable)

A friend of mine in Kota took ₹3,000 from an instant loan app during exam time.

He thought, “2 weeks mein de dunga.”

But:

- No income came

- Late fees started

- Calls increased

In the end, he paid around ₹4,200.

His exact words:

“Loan chhota tha, tension bada ho gaya.”

That sums it up perfectly.

Depreciation & Long-Term Impact

This is something most articles ignore.

Financial Depreciation

If you keep using apps like Pocketly:

- You lose money in fees repeatedly

- Your monthly expenses increase silently

Small loans = big cumulative loss.

Credit Behavior Impact

Two scenarios:

✔️ If you repay on time:

- Credit score improves

- Financial trust builds

❌ If you delay:

- Credit score drops

- Future loan chances reduce

Psychological Cost

This is real.

Frequent borrowing leads to:

- Stress

- Dependency on loans

- Poor money habits

Over time, your financial discipline declines.

When You Should AVOID It

❌ For shopping, gadgets, or parties

❌ If you don’t have repayment plan

❌ If you’re already in debt

Be honest with yourself here.

Smart Alternatives for Students in India

Before using Pocketly, consider:

- Borrowing from family (no interest, no stress)

- Part-time work (freelancing, tutoring)

- Using savings apps

- College emergency funds (many institutes have this)

Sometimes the “boring option” is the safest.

FAQs (Students Ask These a Lot)

1. Is Pocketly RBI approved?

Pocketly works with RBI-registered NBFC partners, but the app itself is not a bank.

2. Can students without income use Pocketly?

Yes, but repayment responsibility is still yours.

3. What happens if I don’t repay?

Late fees, calls, and possible credit score damage.

4. Is Pocketly better than KreditBee or mPokket?

All are similar—differences are minor. Risks are almost the same.

5. Does it affect CIBIL score?

Yes. Timely payment helps, delays hurt.

6. Is my data safe?

Generally safe, but permissions (contacts/SMS) raise concerns.

7. How much interest does Pocketly charge?

It varies, but effective cost can feel high due to fees.

8. Can I extend repayment?

Sometimes yes, but extra charges apply.

9. Is it good for first-time borrowers?

Only if used responsibly and rarely.

10. Should I rely on it regularly?

No. That’s where most students get trapped.